A symposium entitled: Random walk tests for the MENA stock returns

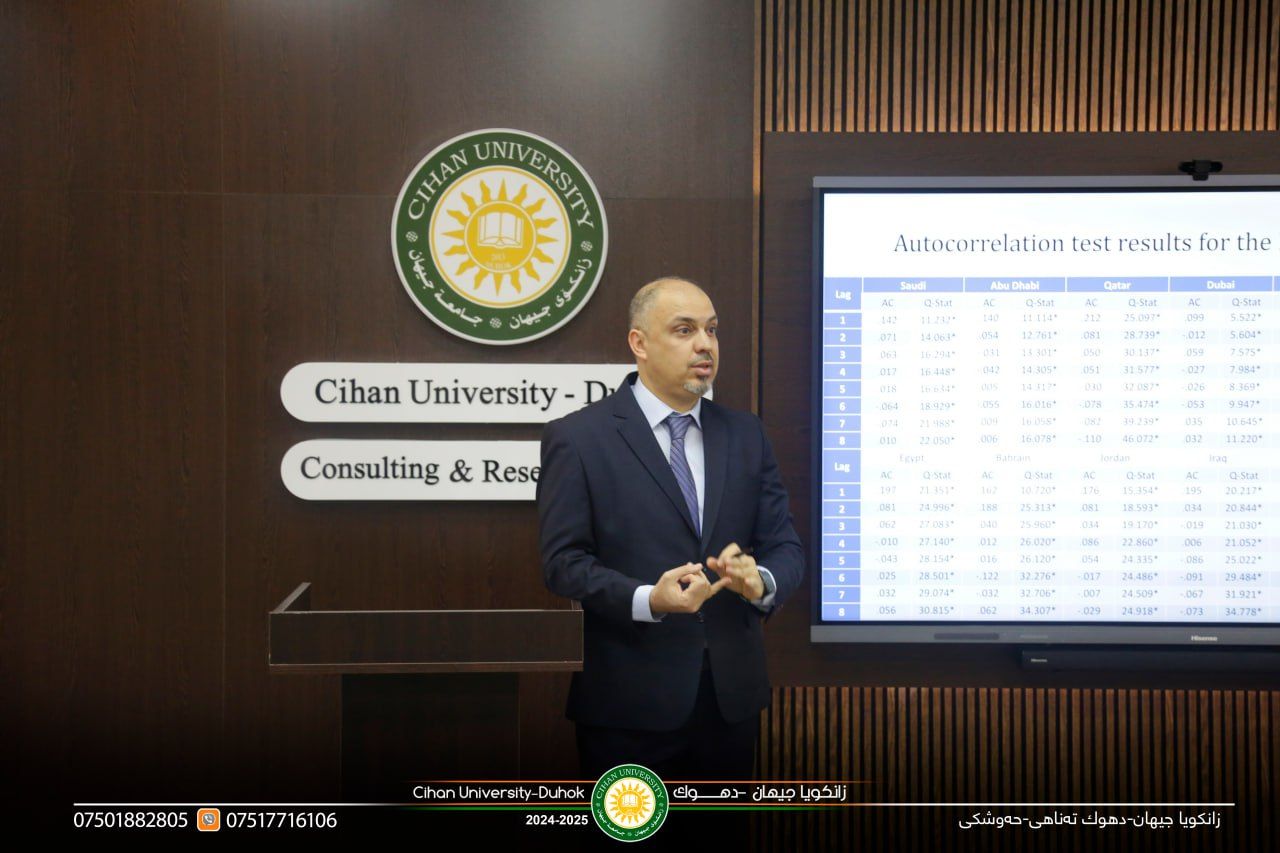

Today on (Oct 10, 2024) in the presence of the vice president for scientific affairs Assist Prof. (Dr. Bayar Mohammad Rasheed) also in the presence of the head of departments and lecturer a symposium entitled (Random walk tests for the MENA stock returns), was presented by (Prof. Dr. Zeravan Abdulmuhssen Asaad) the President of Cihan University - Duhok, Where it has been explained about The current study seeks to understand whether individual stock returns exhibit random movement and are not dependent (efficient at weak form) on fourteen out of sixteen actively traded Arab stock markets in the Middle East and North Africa (MENA) region, based on the size of the market value. Various non-parametric methods, including autocorrelation test, variance ratio test, Phillips-Perron unit root test, and runs test, are used to assess the random walk hypothesis for daily data following the Covid-19 vaccination program. This analysis covers the period from January 3, 2021, to March 28, 2023. The study results present evidence that all individual stock returns deviate from random walk behavior. However, only Kuwait, Jordan, and Palestine stock returns follow the random walk based on the run test results at a significance level of 10%. Therefore, it can be concluded that all stock returns are inefficient at the weak-form, suggesting that investors have opportunities for unexpected gains., a set of questions and answers were raised on this subject